When I was doing my NS, I wasn’t exactly very frugal with my money.

Think plenty of taxi rides, food delivery, and going out with friends.

For many NSFs, it was probably a similar situation. After all, between being stuck in camp during weekdays, and feeling fatigued on the weekends (if you even get to book out), it’s natural to spend more money for convenience.

Six years after I ORDed, I feel a tinge of regret for not being more careful with my money and seizing the opportunity to become more financially fit early on in life.

If I could turn back time and do things differently, I would be one step closer to my ultimate dream: retiring early, and saying goodbye to the corporate slog.

This is why.

I wish I stuck to the free things in NS

After going through university, and having worked a full-time job for two years, I realised that NS is actually the best time to save money.

Why? Because most of the things I really needed in NS were completely free.

Food? Go eat at the cookhouse, along with everyone else. Fall sick? Medical care is free, courtesy of the SAF. Daily transport? Lucky you stay in camp!

Unfortunately, while I could have optimally saved a lot of money during my own NS days, I fell into a financial trap just like many others before.

I ate at the canteen really often, paying and binging on generous portions of food rather than eating it free at the cookhouse. And whenever I felt too tired to take public transport (which was unfortunately way too often), I chose to take taxis, which took up a huge chunk of my allowance - reasoning to myself that it wasn’t that expensive, and was totally worth it.

In hindsight, all of the money I spent not eating the free food and taking public transport really adds up.

I also splurged whenever I hung out with my army buddies, figuring that I was too young to be worrying about saving money, and that I had plenty of time to do so in the future (obviously, I regret that quite a bit now).

Wish I didn’t procrastinate

Looking back, I wish I didn’t procrastinate on saving money while I was in NS.

I’m at a stage of my life where there are an increasing number of bills to pay, with more to come in the future.

Having to pay off student loans is one thing, while having to save up for a wedding, house and possibly kids in the future is a whole different level in terms of difficulty.

While I’m still able to save a decent amount of money each month, I only began saving diligently after I started working, and exercised greater financial prudence.

My NS and schooling years, which would have been a great time for me to start saving for my future, were essentially wasted.

Coupled with the fact that I’ve been putting my savings into a standard bank account for the first 25 years of my life, earning measly returns, I realised that I needed to act quickly, if I ever wanted to retire early in Singapore.

Consider signing up for Singlife

After doing some research, and sieving out all the shady get-rich-quick schemes that are abundant on the internet, I realised that my next move was clear: I needed to invest my money.

With inflation hovering at about 2 per cent per annum, maximising your savings is not enough to achieve financial freedom; after all, the value of your savings will only erode, slowly but surely.

However, while I was determined to start investing, figuring out how to do so proved to be more difficult than I originally anticipated.

There are many decisions I have to make, all of which would directly affect my precious savings.

What trading platform do I use? What should I invest in? Do I even know what I’m doing?

Luckily, if you’re relatively new to investing like me, there are many options in the market to help you dip your toes into the world of investing.

For instance, you can consider Singlife Sure Invest: an investment-linked policy (ILP) that offers both investment opportunities and insurance protection.

You can choose between three different investment profiles, depending on your risk appetite, and Singlife Sure Invest will handle the rest.

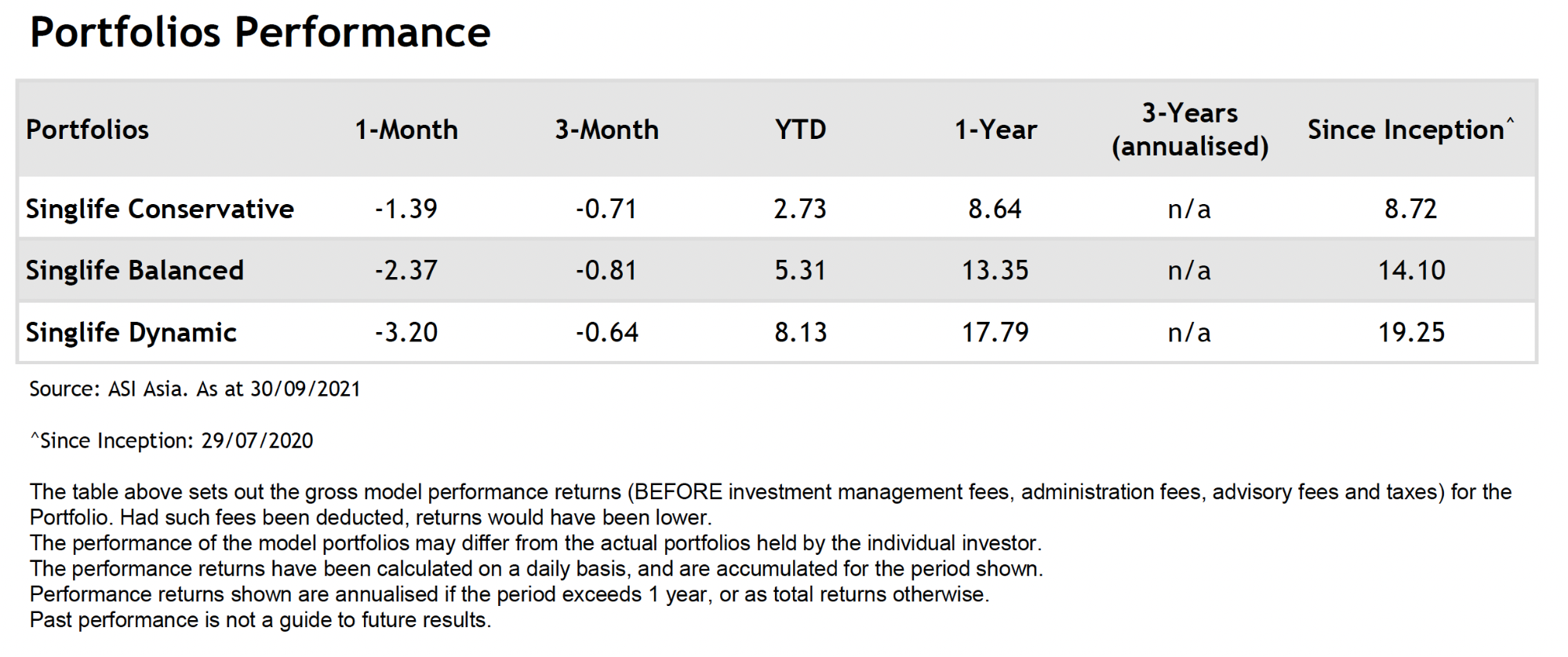

Singlife Sure Invest’s portfolios are managed by global asset management company abrdn Asia Limited (previously known as Aberdeen Standard Investments), and while investment returns are not guaranteed, they are likely to be higher than most savings accounts, provided you are comfortable with the risks involved.

For example, if you’ve been on Singlife Sure Invest since September last year, your returns range from 8.64 per cent to as high as 17.79 per cent^.

However, if you prefer not to invest your money for now, it doesn’t mean there aren’t any ways for you to grow your money.

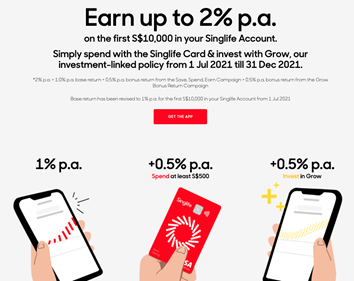

For example, the Singlife Account gives you up to two per cent return per annum, on your first S$10,000 when you participate in their bonus return campaigns*, and 0.5 per cent thereafter, up to a limit of S$100,000.

This is not a traditional bank account; it’s an insurance savings plan that is capital guaranteed, with the value in the Singlife Account protected up to a specified limit by the Singapore Deposit Insurance Corporation.

However, unlike many longer-term insurance savings policies, you can withdraw your money at any time, and there’s no minimum lock-in period.

Best of all, Singlife is currently running a referral campaign, where Singlife customers are rewarded for inviting their friends.

Current and new Singlife customers who successfully refer friends will receive S$5 into their Singlife Account, when referees sign up for the Singlife Account and activate their Singlife Debit Card.

Customers will also be rewarded with an additional S$30 when their friends sign up and fund their first Singlife Sure Invest policy after.

There are no limits to the number of referrals, so you can refer as many people as you like. If you don’t have a referral code to use, you can sign up for the Singlife Account or ask around.

I had fewer options back in the day

To be honest, I’m a little jealous.

During my NS days, there were simply fewer options for someone like me to earn higher returns on my savings.

Various banks offered savings accounts that promised similar interest rates, although I did not qualify for them, as many of them required me to credit my monthly salary (I had no salary), or to spend a certain amount per month on the bank’s credit card (I cannot apply for a credit card with no salary).

I distanced myself from fixed deposit accounts, or insurance savings plans with a lock-in period, as I felt uncomfortable with locking away my money for long periods of time.

Products like Singlife Sure Invest would have allowed me to start my investment journey way earlier, and helped me grow my money at a younger age.

This would have allowed me to pay off my student loans, and brought me closer to affording my own house.

After all, starting as early as possible matters.

Hypothetically, if I invested S$500 a month, from the age of 30, I would end up with around S$336,000 at the age of 60, assuming returns of 4 per cent per annum with compounding interest.

If I invested the same amount from the age of 20 instead, I would end up with a staggering S$570,000 instead.

Looking back, spending on those plates of food might have cost me several more years of work.

Top image via MINDEF/FB and Unsplash.

This sponsored article by Singlife made the writer realise that taking a taxi everywhere during his NS days was a huge mistake.

*2% p.a. = 1.0% p.a. base return + 0.5% p.a. bonus return from the Save, Spend, Earn Campaign + 0.5% p.a. bonus return from the Singlife Sure Invest Bonus Return Campaign

*Note: Singlife Account’s base return is 1% p.a. on first S$10,000 & 0.5% p.a. on amounts above S$10,000. There are no returns for amounts above S$100,000. Returns are not guaranteed.

^Figures represent gross model performance returns before deduction of fees. Return is calculated on a daily basis, accumulated for the period shown. The performance of the model portfolios may differ from the actual portfolios held by the individual investor. The performance for your Singlife Sure Invest portfolio is not guaranteed and the value of the units and the income accrued to the units (if any) may fall or rise. Past performance is not a guide to future results. You can purchase multiple policies, with one portfolio per policy.

The views and opinions in this article are those of the author and do not represent or reflect the views of Singlife. The information is meant for your general knowledge and does not regard any specific investment objectives, financial situations or particular needs any person might have and should not be relied upon as the provision of financial advice. This advertisement has not been reviewed by the Monetary Authority of Singapore. Protected up to specified limits by SDIC. Information is correct as of 15 November 2021.

If you like what you read, follow us on Facebook, Instagram, Twitter and Telegram to get the latest updates.