News

S'porean woman, 43, suffers 5 brain aneurysms, has insurance claim rejected by Prudential but approved by AIA

What's in an insurance policy?

March 28, 2026, 11:04 AM

In July 2024, Molly Chiang (not her real name) went to the hospital.

She'd been having a bad headache. A few scans later, she learnt that she had five aneurysms in her brain.

She was 43 years old.

A brain aneurysm is essentially a swollen blood vessel. If it bursts or ruptures, it causes a hemorrhagic stroke — the less common, and deadlier, kind of stroke.

Chiang was told that her aneurysms could burst any time. If any of them did, she had a 50 per cent chance of death, and a 50 per cent chance of entering a vegetative state.

She needed emergency surgery. Her doctor said he would do the procedure endovascularly.

It was less risky, less invasive, with a quicker recovery time, he explained.

"For me, I just went 'sure, OK'... I mean, as a layman, I didn't know what it was, right? I'm no medical expert.

I trusted the doctor. That was the recommended way of treatment for my condition... He's a specialist in this field, in Singapore.

So I just went with it."

In the end, Chiang had to go for two surgeries, because of the number of aneurysms. They were a success. The doctor, as far as she could tell, had been right.

She recovered, was discharged, and is today aneurysm-free.

The problems would only start later, when she tried to file an insurance claim.

Fine print

On Mar. 18, a woman went to trial with insurance provider Prudential over a brain aneurysm surgery.

Cai Yanhong, 45, had a stroke in 2023. Like Chiang, she was recommended an endovascular repair. Like Chiang, she agreed, underwent the surgery, and recovered.

But when she tried to file a claim under her Prudential critical illness (CI) policy, it was denied.

According to Prudential's policy definitions, brain aneurysm surgeries are only claimable if they are done via surgical craniotomy, not endovascular repair.

The former is an open-skull procedure, whereas the latter is widely described as "minimally invasive".

During the trial, Cai said that she was not given a choice as to what surgery would be performed, and that the craniotomy was riskier, more invasive, and had higher mortality rates.

But Prudential argued that the contract had "made it very clear" that the surgery Cai underwent was not covered in the policy.

"In essence, Ms Cai’s case is that the terms of the contract between the parties ought to somehow be what she likes them to be, as opposed to what had been expressly agreed in writing between the parties," lawyers for the firm said.

A similar experience

As it turns out, Chiang had a similar experience — with one key difference.

Back when she was buying her critical illness insurance, she decided to purchase two policies.

One was with Prudential, and one was with AIA.

Both policies are essentially similar in that they're both early CI insurance policies with "quite high premiums".

"For my family, I'm a single-propeller plane," Chiang explained. "I do a lot of financial support for my sisters, as well as my mum."

"So I wanted to be extra protected... Buy a bit more, if anything happens to me, if I die, my family has money to live on."

After her surgeries, Chiang filed claims under both policies. That was at the end of last year.

She sent over the same documents, the MRI scans, the doctor's reports, essentially duplicates of the same claim.

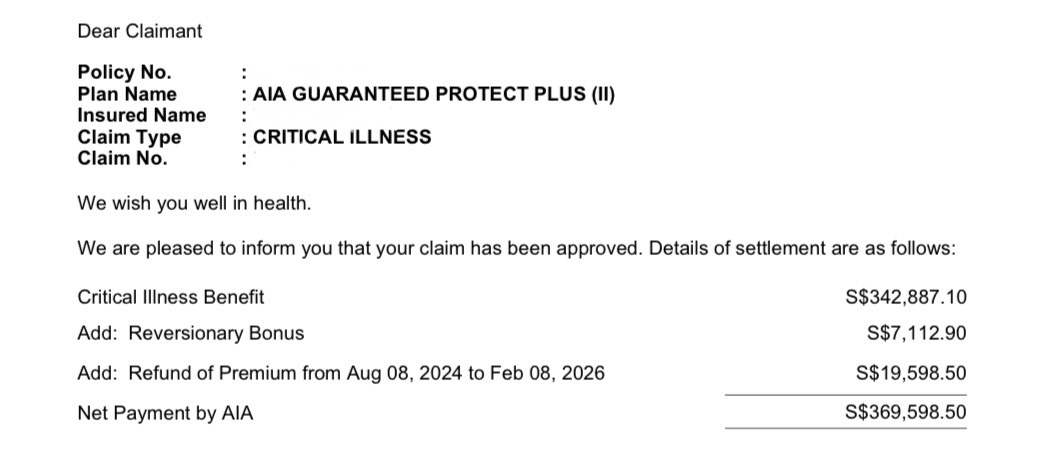

A few months later, AIA paid her the money.

But Prudential denied her claim.

The difference

Chiang showed Mothership copies of her correspondence with both AIA and Prudential.

In rejecting her claim, Prudential cited the same reason as they did in Cai's case: that endovascular surgeries are not covered in the CI policy.

From AIA.

From AIA.

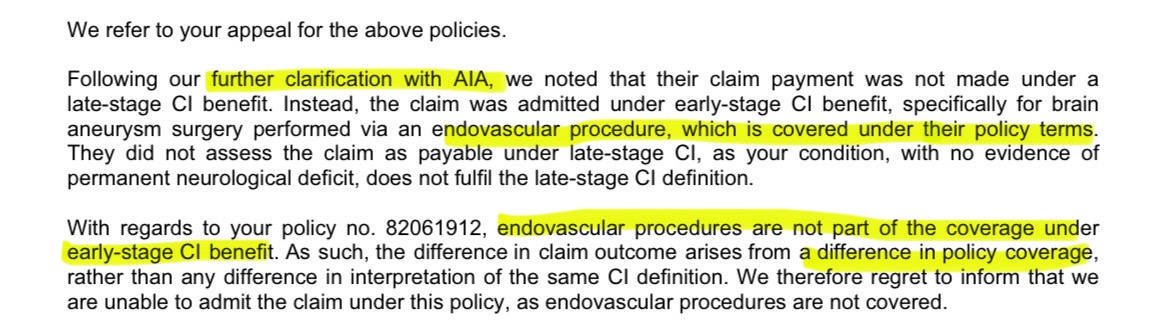

From Prudential.

From Prudential.

At first, Chiang was incredulous.

She filed an appeal with Prudential, explaining that AIA had approved her claim.

"[I said] I don't understand why, under the similar coverage, under critical illness, why you do not cover," she said.

What followed was some back-and-forth. Prudential asked her to provide information on her settlement with AIA, which she did.

A few days later, Prudential replied to her with this:

"They still said no, because they said their definition clearly excludes endovascular procedures," Chiang said.

Buyer and seller

One thing from Cai's trial that Chiang took issue with was the question of whether such an exclusion is market practice.

Cai had alleged that other, rival insurers did not specify the need for a particular type of procedure, when defining the condition of a brain aneurysm.

In response, Prudential said that it was not a "market outlier" and called her claims "disingenuous and false".

But Chiang pointed out that from her own experience, AIA did indeed have a broader definition.

"I don't know how Prudential covers other things," she said.

"But for me, for this particular condition, AIA definitely performed their duties as an insurer, which is to give you protection, given the condition.

[Whereas] Prudential specifies that you have to go through a certain type of treatment before we pay you."

Signing a contract

Chiang added that prior to her illness, she had similar experiences with both insurance agents from AIA and Prudential.

Both agents went through the policies in similar levels of detail, without paying exhaustive attention to the exclusions.

"Obviously, they didn't highlight that for this particular critical illness, there are exclusions... or for that condition, our bar is set higher than other insurers. They don't do anything like that," she said.

"I signed off on it, hand on heart. That was a contract, sure.

But I pay these premiums so that I get protection. That's the whole point."

Chiang added that she's sharing her story to raise awareness of this issue.

"A lot of people don't have the means to go to court or to tell anyone. And they just suffer in silence because they don't know any better," she said.

"[Cai] and I might not win. But at least people know."

Insurers' responses

A spokesperson from AIA Singapore said it was unable to comment on "individual cases or competitors".

It added:

"Broadly speaking, insurance coverage offered by insurers can differ for a range of reasons, including the timing of policy purchase and the medical practices in place at that time."

Prudential declined to respond to Mothership's queries when contacted.

Top image from AIA and Prudential/Google Maps