If you're not getting a S$850 GST voucher, who is? And why does your home's 'annual value' matter?

Explaining the August 2024 GST voucher.

By

Nigel Chua

July 31, 2024, 02:46 AM

Singaporeans' love for their country generally gets stirred up in August.

Fireworks, festivities, Singapore-themed offerings at F&B outlets, and discounted prices for various things (like prices getting slashed to S$5.90 to celebrate Singapore's 59th national day).

But that's not the only piece of good news for Singaporeans this August.

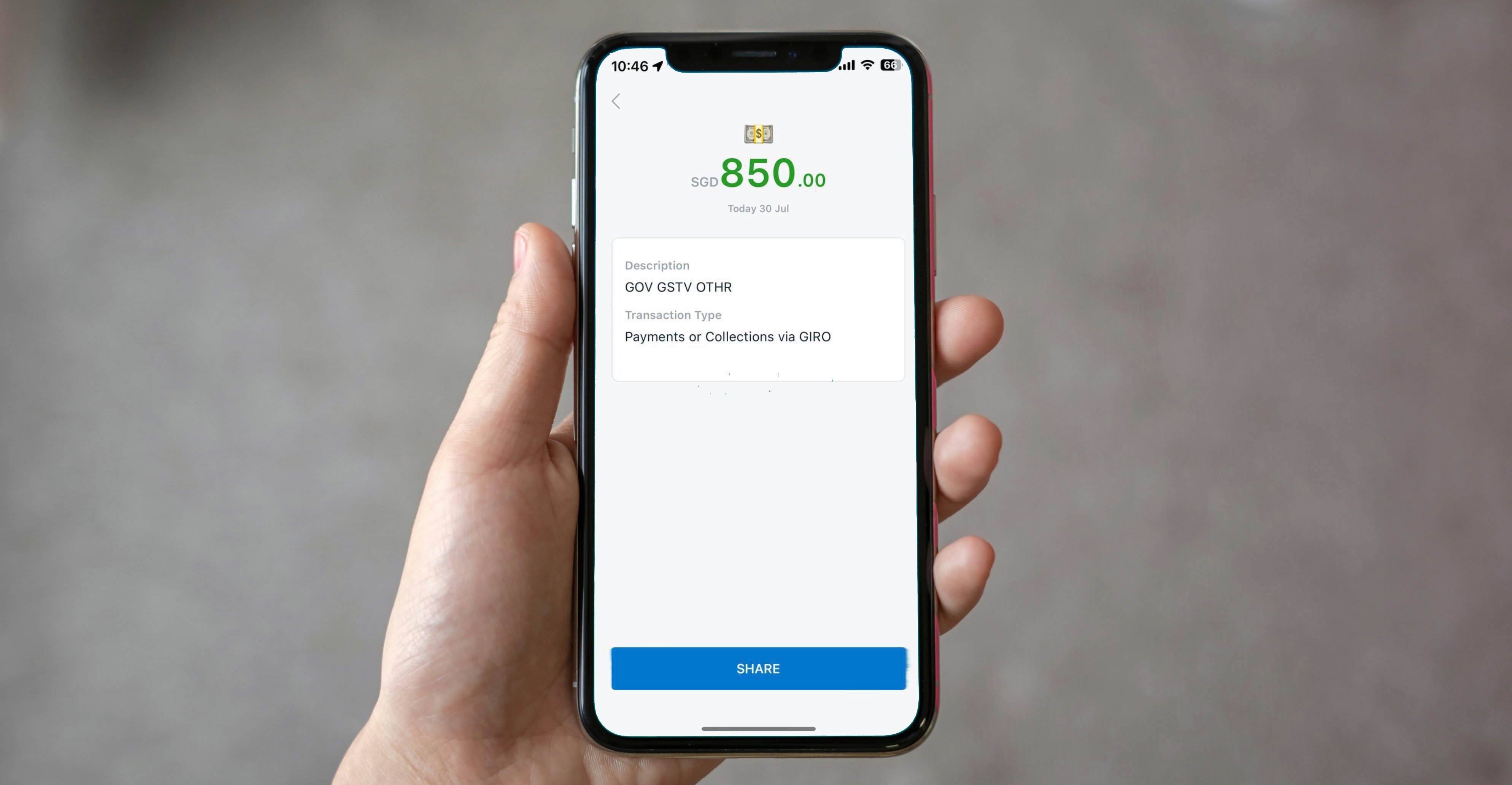

Many of them, who are fluent in the love language of money, would also have extra reason for cheer thanks to the GST voucher (GSTV) — and for some, S$850 of GSTV in cash.

Screenshot via govbenefits.gov.sg.

Screenshot via govbenefits.gov.sg.

But wait, what does GSTV have to do with GST?

The govbenefits website explains that GST vouchers provide help to lower- and middle-income Singaporean households and seniors.

The GSTV is not to be confused with other direct transfers from the government, such as the 2018 "SG Bonus" benefit of S$100 to S$300, as well as the 2020 "Solidarity Payment" and "Care and Support – Cash payment", between S$300 and S$900, with amounts depending on one's assessable income in the relevant years, and one's property ownership.

Instead, the GSTV — as its name suggests — has more to do with Goods and Services Tax (GST).

Here's the link between GST and GSTV:

GST is an important source of government revenue, amounting to S$14.1 billion (or 20.5 per cent of the total S$68.6 billion of tax collected in financial year 2022/23, according to IRAS's most recent annual report).

However, the burden of paying this 9 per cent consumption tax can be a heavy one, especially for lower-income groups, and thus, GSTV helps to alleviate that burden somewhat.

MOF says the GSTV is "fairer and more effective", as compared to the alternative options, such as implementing a multi-tier GST system (where those who earn less pay less GST), or not imposing GST for basic necessities.

GSTV was made a permanent scheme in 2012, and today, it has four components: Cash, MediSave top-ups, offsets for utility bills, and rebates on Service & Conservancy Charges (S&CC).

The GSTV cash payout this year is limited to 1.5 million Singaporeans, roughly a quarter of the population.

You may or may not be a GSTV recipient this time around.

So, who doesn't get GSTV in cash?

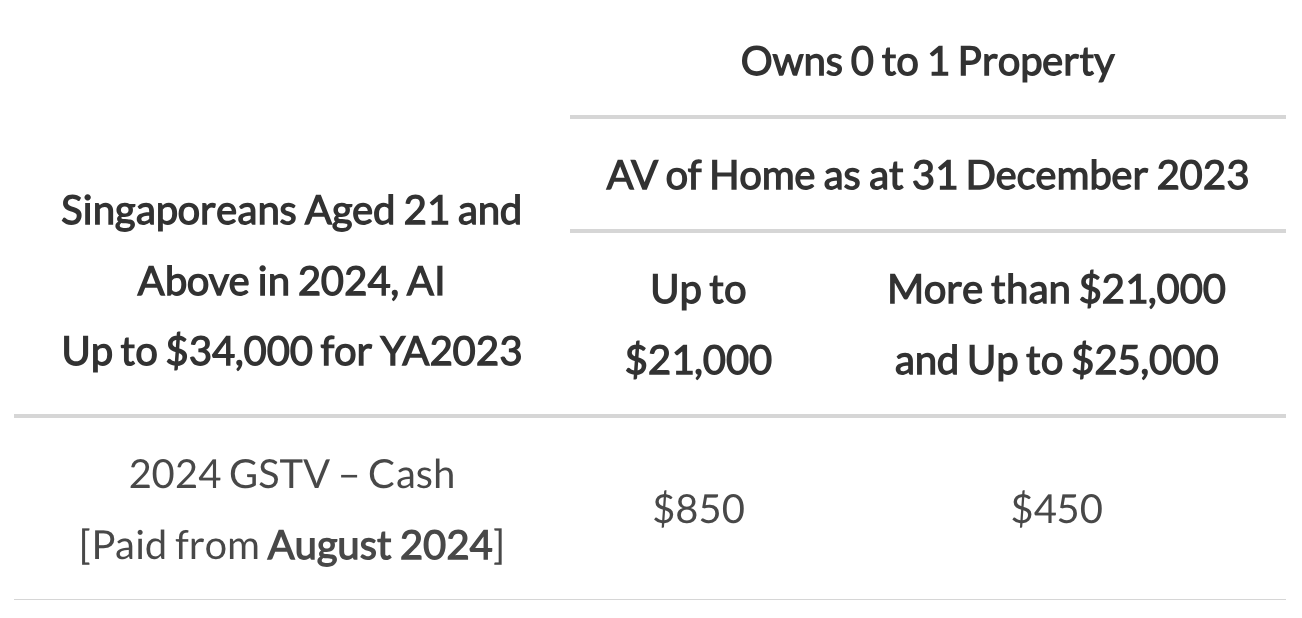

Let's assume that you're a Singaporean, that you're residing in Singapore, that you're 21 and above in 2024, and that you don't own more than one property — all criteria for receiving the GSTV.

If all that is the case, then the two easiest ways to be disqualified from GSTV cash payouts are: Earning more than S$34,000, and having an Annual Value of Home (AVH) of S$21,000 or more.

>S$34,000 income earned in 2022

If you're not eligible for GSTV this round, it could simply be that you earned more than S$34,000 of assessable income in the Year of Assessment 2023 (or, your "YA 2023 AI", in typically-Singaporean acronym form).

Simple math: S$34,000 works out to around S$2,833 per month, so if your monthly salary is at least that, no GSTV cash payout for you.

Note that your YA 2023 AI isn't what you earned in 2023.

Rather, it's what you earned in 2022.

This is because the Inland Revenue Authority of Singapore (IRAS) only assesses your income the year after it is earned.

"Can't CPF contributions serve as quick and relatively-foolproof evidence of one's income?", you might ask.

But, that wouldn't be able to capture other income sources such as rental income, or the incomes of those who are self-employed and who may not have CPF contributions.

In other words, yes — there is a one-year lag in assessing how much you really need the cash assistance from GSTV, but if there's a more efficient or faster way of finding out how much Singaporeans are earning, IRAS would definitely want to know.

Annual Value of Home (AVH) S$21,000 or more

Another key criteria that would make some Singaporeans ineligible to get the GSTV is Annual Value of Home (AVH) — or, the estimated gross annual rent of the property where they live, if it were to be rented out.

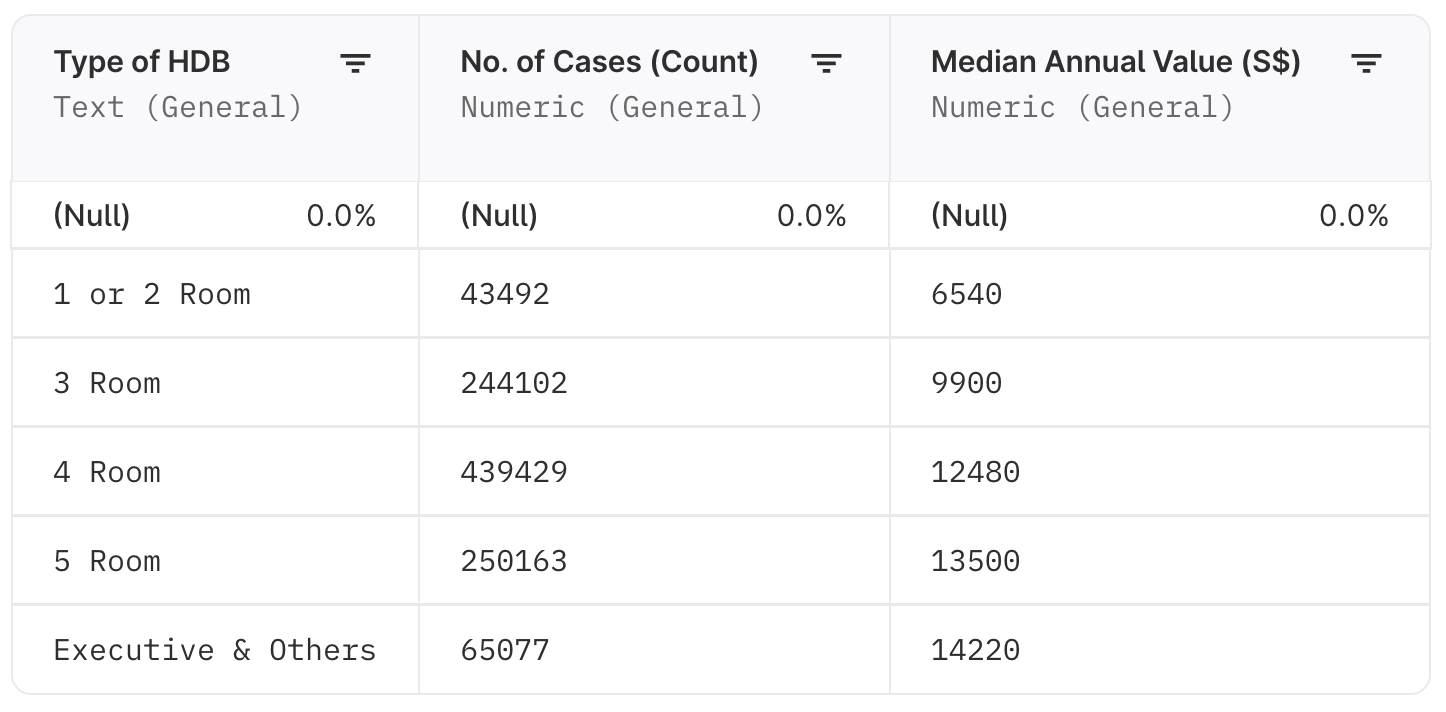

The median AVH for a four-room flat in 2022, according to data.gov.sg, is S$12,480, which works out to S$1,040 a month.

But, as IRAS explains, AVH factors in "a reasonable allowance" for things like furniture, furnishings, and maintenance fees and is thus lower than the actual rental rate.

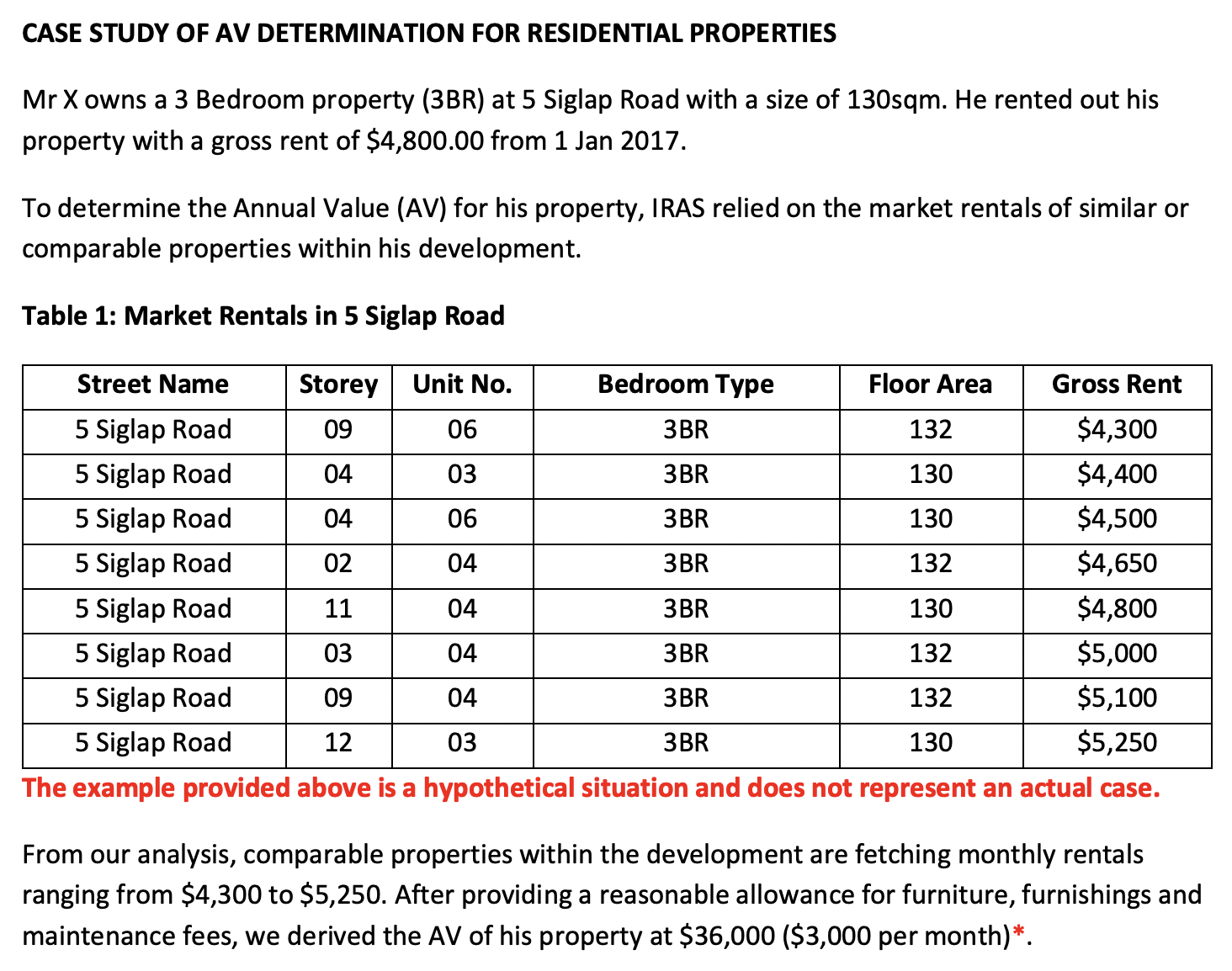

Here's a case study the tax authority created to explain this, in which a property rented out for S$4,800 monthly is given an annual value based on S$3,000 per month:

Screenshot via IRAS's "Case study of AV determination for residential properties".

Screenshot via IRAS's "Case study of AV determination for residential properties".

Here's the median AVH for different types of HDB flats in 2022:

Screenshot via data.gov.sg.

Screenshot via data.gov.sg.

Why does this number determine your eligibility for this lucrative government benefit of cash with no strings attached?

The short answer is that it's an efficient way of gauging how wealthy someone (and their family) is. The lower the AVH, the more likely the person (and their family) will be in greater need of financial support.

It's straightforward because it zooms in on residential property — likely to be the largest asset a household owns — and uses that as an indication of wealth, instead of trying to capture all of the household's assets (which may include hard-to-value assets like cars, watches, jewelry, rare Pokemon cards, etc.).

It's efficient, because the AVH of homes in Singapore are already calculated each year (as it determines how much property tax the owners must pay).

Here's more, from an MOF spokesperson in 2022:

"There are individuals who may not deriving much income, but have substantial savings or good access to family support. This is why we also look at the Annual Value of the property (“AV”) that the individual lives in, as well as whether the individual owns more than one property, to assess how well-off the individual and his/her family may be."

The spokesperson also added that one's assessable income and AVH are "proxies" that "provide an efficient way for the government to determine eligibility for the GSTV using available data, without requiring citizens to apply individually".

There are some who may be in need due to "extenuating circumstances", but do not meet the criteria, the spokesperson noted. They can write in to MOF and their situation will be assessed "on a case-by-case basis", said MOF.

Other cash payouts

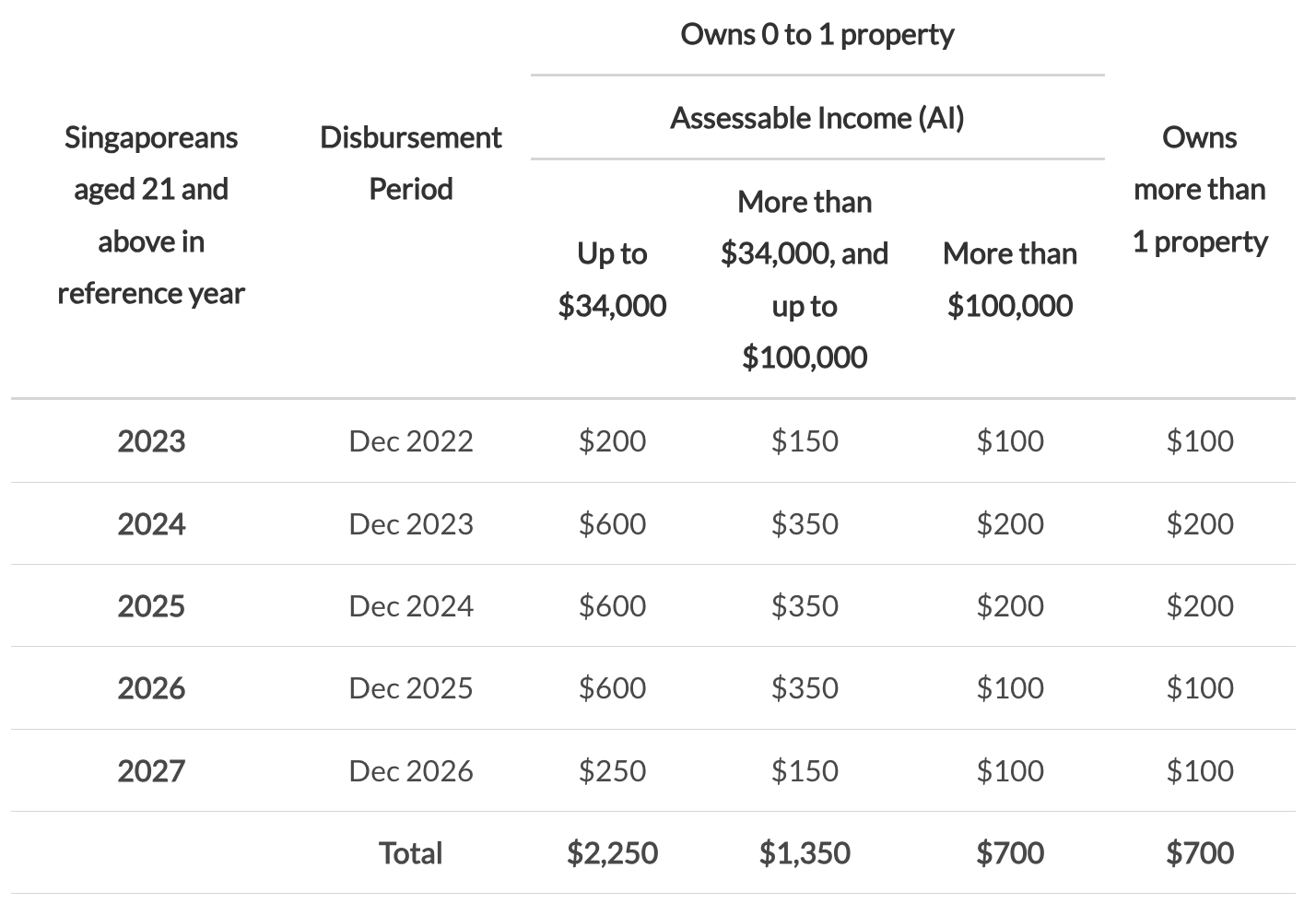

Even if you didn't get the GSTV this time around, there are other cash payouts you may be eligible to receive, such as the Assurance Package Cash Special Payment, also known as AP Cash, as well as the Cost-of-Living (COL) Special Payment.

AP Cash (to be disbursed in December 2024)

Every Singaporean aged 21 years and above will receive cash payments of between $700 to $2,250, depending on his/her income and property ownership.

The payments will be disbursed over five years, from 2022 to 2026, as follows:

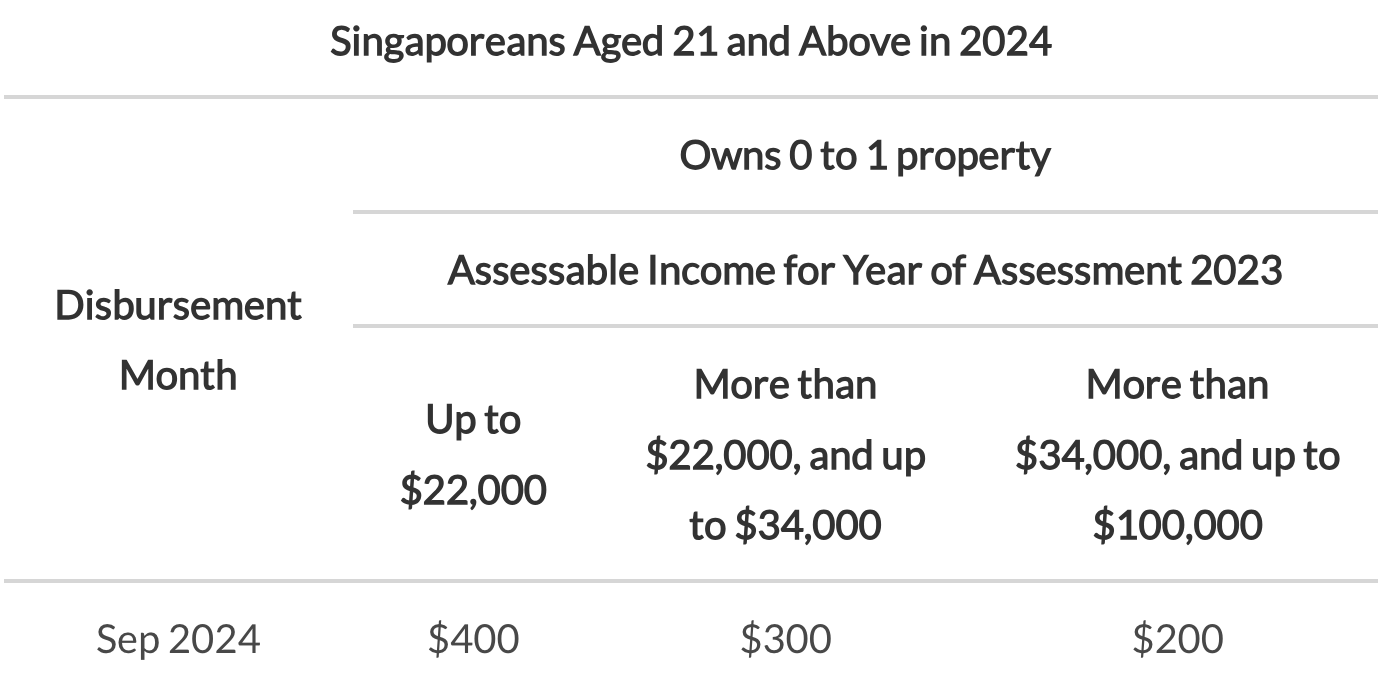

Cost-of-Living (COL) Special Payment (to be disbursed in September 2024)

As part of the enhanced Assurance Package announced at Budget 2024, eligible adult Singaporeans aged 21 and above in 2024 will receive one-off special payment amounting to between $200 to $400 in cash, depending on their income and property ownership, in September 2024.

LifeSG credits (to be disbursed in November 2024)

If you're an NSman or a full-time national serviceman, you can expect to get S$200 in LifeSG credits in November 2024.

Not exactly cash, though there are ways of converting the credits to cash.

Top photo via Mothership reader and by CoinView App on Unsplash