Follow us on Telegram for the latest updates: https://t.me/mothershipsg

This year marks the 40th anniversary of GIC.

GIC is commemorating this milestone with a series of "bold stories" from their publication, Bold Vision: The Untold Story of Singapore’s Reserves and Its Sovereign Wealth Fund.

Here, we reproduce an excerpt from Chapter 3, outlining the history of how a young nation stood against conventional wisdom when introducing the Singapore dollar.

You can get the book here, or listen to the audio version on Spotify.

Singapore issued its own currency on June 12, 1967.

The conventional wisdom then was that it should have established a central bank simultaneously. Instead, the government chose to maintain what was even then considered an archaic symbol of colonialism – the currency board system.

Far from being quixotic, this decision underlined the young nation’s commitment to the values of thrift and industry. And though the Board of Commissioners of Currency has since merged with the Monetary Authority of Singapore (MAS), which then assumed the function of currency issuance, its establishment in the early years of independent Singapore was to have far-reaching consequences.

It laid the foundations for the country’s rapid accumulation of reserves in the 1970s; and that, in turn, led to the creation of GIC in 1981.

What is the currency board system?

The currency board system was an invention of the British Raj and was designed to ensure that the currencies issued by its colonies were fully backed by sterling reserves held in London.

The system was beneficial to both sides: to Britain, because the capital inflows into London helped the City become the world’s leading financial centre; and to the colonies, because it resulted in stable and convertible currencies.

Paradoxically, having invented a system for the colonies that would be synonymous with currency stability, the British Raj would subsequently be haunted by sterling crises because Britain eschewed a similar system for itself.

The currency board system was almost wholly abandoned by the late 1960s, as the winds of change that blew through Asia and Africa saw almost all of Britain’s colonies attain independence. These countries decided that a central bank would better suit their new status. After all, a currency board system would only have given the governments of these newly independent countries control of the note issue.

What is a central bank system?

A central bank, in contrast, would give them the power to vary the money supply by manipulating bank credit and thus influence economic conditions.

A central bank can ease credit conditions during an economic downturn and tighten them when the economy overheats. It can also create money without it being fully backed by reserves. Of course, most of the newly independent countries did not have money markets of a size and depth to enable monetary policy to work as textbook theory prescribed.

But a central bank – like a standing army or a diplomatic service – was deemed to be something independent countries just had to have. And so they did.

Singapore was advised to follow suit. International Monetary Fund (IMF) missions to Singapore during this period recommended the adoption of a central bank system.

Apart from creating bank credit, a more important component of the money supply than the note issue in advanced economies, a central bank would also be able to be the lender of last resort, the IMF teams advised. Even the individual retained by the Singapore government to be its currency advisor, an RW Goenman, recommended a central bank.

S'pore opts for the currency board system instead

But the Government was unmoved and opted for a currency board. Indeed, it never wavered in believing that it was the only viable option for Singapore.

As Dr Goh was to recall in a speech two years later in 1969:

“The test cabinet decided to apply… was which type of institution would inspire more confidence in the new currency?” The cabinet concluded that there was “little doubt that the currency board would fulfil this requirement better than a monetary authority of the central bank type”.

Singapore’s leaders felt they could not take chances with the new currency. The country had to have a stable and strong currency. That was the precondition of its existence as a financial and commercial centre in the region. With a currency board, traders and investors would know that every Singapore dollar was backed by its equivalent in reserves, and was fully convertible to an internationally acceptable currency at a fixed rate.

The importance of system credibility

Young Singaporeans today might find it difficult to imagine a situation when it was possible to doubt the Singapore dollar. After all, the Singapore dollar has steadily appreciated against all major currencies since its inception. But the circumstances for the Singapore economy and currency were far from propitious in 1967.

First, there was uncertainty as to how the new currency would be received. Second, the country faced an uncertain economic future. And third, as it had separated from Malaysia just two years earlier, there was still a question mark over its viability as an independent state.

Moreover, the currency split with Malaysia had dashed whatever remaining hope there was of a common market with Malaysia. To make things worse, the British government announced in 1967 that it would withdraw its military forces “East of Suez”. About 15 per cent of Singapore’s workforce had jobs linked to British military bases on the island.

As the then-British high commissioner to Singapore telegraphed London:

“It is unfortunate for Singapore that the introduction of the new currency had to follow the announcement of our intention to run down our forces and took place against speculation—fortunately most of it covert as to how the infant republic would be able to contain the economic effects of the run down on top of Singapore’s general economic problems of large and growing unemployment, tardy industrialisation and general lack of export outlets.”

Of course, those who counselled Singapore against a currency board system argued that it was not the system that produced currency confidence. Ultimately, it was policy credibility that secured system credibility. The system cannot substitute for credible policies.

Singapore’s political leadership too subscribed to the importance of policy credibility. But they felt that form and substance were equally important. There should be no doubt about how the Singapore dollar was issued, or about its backing and convertibility. And neither should there be any question about the Singapore government’s determination to do whatever it took to live within its means.

System credibility, they felt, would reinforce policy credibility: the straitjacket of a currency board system was the price the new country had to pay for confidence in the currency.

How the currency board system works

The currency board system works according to mechanical rules. The discipline it imposes on a country is clear but stark. There is no room for policy improvisation. It operates as the gold standard did.

Under the gold standard, trade imbalances led to changes in the stocks of gold countries held and thus their money supply, which then caused changes in the levels of employment, incomes and prices. These variations in turn led to changes in domestic demand for imports and foreign demand for the country’s exports, eventually reducing the trade imbalances and restoring equilibrium.

Similarly, under the currency board system, an adjustment process would be triggered if the country incurred trade deficits repeatedly.

Persistent trade deficits would mean that foreign traders would be holding increasingly large stocks of the deficit country’s currency. As these traders redeemed it for the reserve currency, the country’s stock of reserves would diminish. A falling stock of reserves would in turn mean that the note issue would have to be correspondingly curtailed.

Though the note issue is but one component of money supply, it nevertheless is the fulcrum on which banks create credit. A shrinking note issue would thus ultimately lead to a contraction in credit. A deflationary situation would be set in motion, leading to higher unemployment and lower wages – and ultimately to a reversal of the trade deficit.

The penalty for loss of competitiveness under a currency board system can thus be severe.

Countries that adopt the system have to cope with deflationary situations by working harder and not by creating credit. But this was precisely the message the government wished for Singaporeans and foreign investors to note. Only if the country accumulated more reserves by exporting more than it consumed could monetary conditions be more accommodating.

Singapore’s leaders wished their people to realise there were no shortcuts to prosperity.

Disadvantages of a central bank system

Aside from choosing a currency board system for these reasons, the Singapore government also had an economic rationale for rejecting a central bank system.

Given the openness of the Singapore economy and the high import content of what Singaporeans consumed, Dr Goh concluded that monetary stimulus would have limited impact in lifting the economy during a downturn: most of the stimulus would simply leak abroad through increased imports. As a consequence of this, he observed in 1969:

“The way to stabilise the economy would lie less in monetary than in fiscal measures. During a downturn, it would be possible to mitigate the harsher effects of a recession if the government were to run budget deficits financed not by central bank credit creation but by spending accumulated overseas assets or proceeds of foreign loans raised on the collateral of these assets. But this would imply the accumulation of such funds during good times… And for this we don’t need a central bank, as the instrument for such measures of stabilization would be the normal government budget.”

The other reason why the cabinet eschewed a central bank was that the central bank’s power to create credit had been frequently abused. Singapore’s leaders had witnessed how the replacement of currency boards with central banks in many newly independent countries had led to inflation and currency debasement.

They had also seen how monetary policy in developed countries, in Lyndon Johnson’s America as well as Harold Wilson’s Britain, had an inflationary bias. “Lead us not into temptation…” – Singapore’s founding leaders did not think they should tempt themselves or their successors with seemingly easy options.

History offers support for their instincts about the value of a currency board system in instilling confidence in the currency.

In 1982, the Hong Kong dollar faced a crisis of confidence following the announcement of the colony’s transfer to China in 1997. A currency board system was installed, with the Hong Kong dollar pegged at HK$7.2 to one U.S. dollar. That squashed speculative attacks against the currency.

Today, Hong Kong still abides by the system, which has kept its currency steady through various crises, including the 1997-98 Asian Financial Crisis, when so many other currencies fell like ninepins.

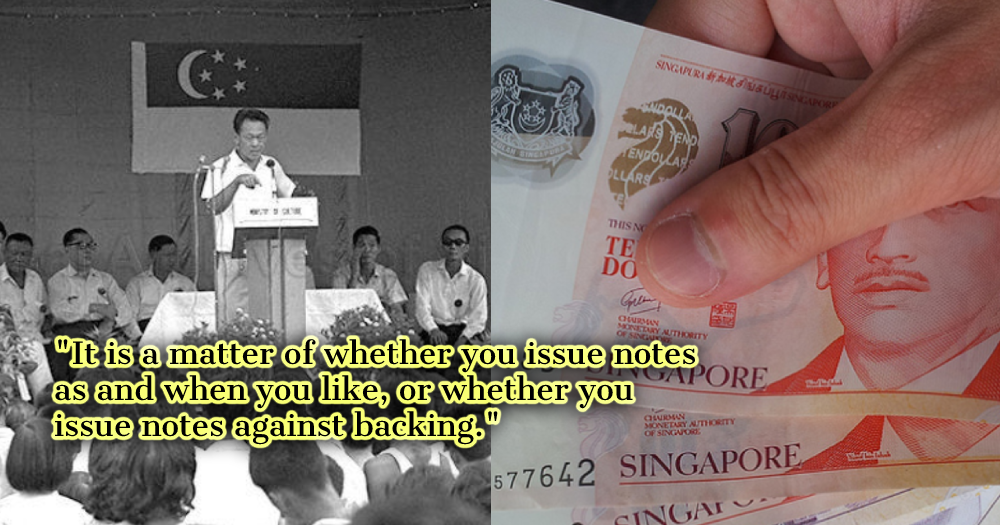

LKY addresses Singaporeans

On August 25, 1966, the prime minister explained to Singaporeans why the country was adopting a currency board system.

A week had passed since the announcement that the common currency talks with Malaysia had fallen through. Singaporeans had yet to be told about what would replace the Malayan dollar and there was some unease about how the new Singapore dollar would fare.

There had been speculation in some quarters, Lee Kuan Yew told his audience, the Singapore General Printing Workers’ Union, that “Singapore is finished, because we have no natural resources”, and so its currency would be weak. But the strength of a currency did not depend on whether a country had vast or slender natural resources.

“It is a matter of whether you issue notes as and when you like or whether you issue notes against backing”, he told the printing workers.

“For every dollar we issue, there will be a currency board which guarantees that there is that amount in gold or foreign exchange in London or New York or some other place to back it. So the money won’t go down”.

Then he added characteristically: “But I will tell you what will go down—employment will go down if you don’t work hard.”

The next day, on August 26, finance minister Lim Kim San announced in parliament the formation of the Board of Commissioners of Currency, Singapore (BCCS). It began operations on April 7, 1967 and issued its first notes and coins in June.

Follow and listen to our podcast here

Top photo via NAS, Flickr user Alexsandr Zykov.

If you like what you read, follow us on Facebook, Instagram, Twitter and Telegram to get the latest updates.